.png)

When high-value or time-critical goods take to the sky, the financial stakes climb right alongside them. A single incident, whether damage during loading, theft at a stopover, or loss in transit, can translate into significant financial losses for your business and your client relationships. That's why having cargo insurance explained clearly matters to every freight forwarder and logistics professional arranging charter flights.

At CharterSync, we help you book air cargo charters with full transparency and technical certainty. But securing the right aircraft is only part of the equation. Understanding how cargo insurance protects your shipments, and where gaps might exist, is equally critical to managing risk effectively.

This article breaks down what cargo insurance covers, the common exclusions you should watch for, and how to navigate the claims process when things go wrong.

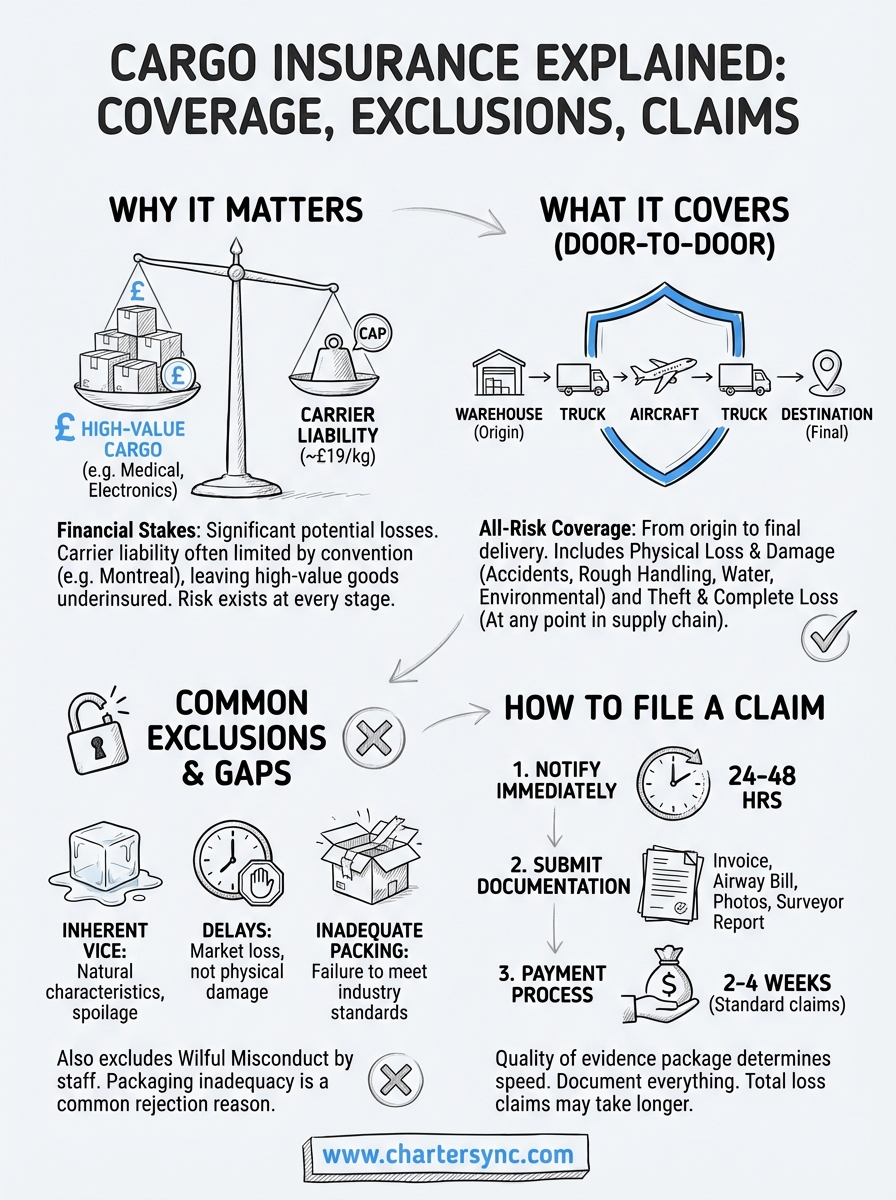

Your business reputation hinges on safe, timely delivery, but the reality of air cargo operations is that risks exist at every stage. From ground handling mishaps at the airport to turbulence during flight, even the most carefully arranged charter can encounter unexpected incidents. Without adequate insurance, you're left exposed to financial losses that can run into hundreds of thousands of pounds, depending on the cargo value.

A single damaged pallet of medical equipment or electronics can trigger claims that exceed the cost of the charter itself. If you're moving automotive parts worth £500,000 and a forklift punctures the packaging during offload, you need to know who covers that loss. The same applies to theft at transit points or damage from improper securing during flight.

Most freight forwarders underestimate the scale of potential liability until something goes wrong. Clients expect you to deliver their goods intact, and when you can't, they'll hold you accountable. Cargo insurance explained in practical terms means having a financial safety net that protects both your client relationships and your own cash flow when incidents occur.

Without proper cover, a single loss can wipe out months of margin on profitable routes.

Standard carrier liability limits are set by international conventions such as the Montreal Convention for air transport, which caps compensation at approximately £19 per kilogram. If you're shipping high-value pharmaceuticals or precision instruments, that statutory limit leaves you massively underinsured. You need dedicated cargo insurance to bridge the gap between what carriers pay and the actual replacement value of lost or damaged goods.

Relying solely on carrier cover also means navigating complex legal frameworks and potentially lengthy disputes. Cargo insurance provides faster resolution and clearer recovery paths, so you can settle claims and maintain client trust without protracted negotiations.

Your cargo insurance policy typically provides all-risk coverage from the moment goods leave the warehouse until they reach the final destination. This means protection against physical loss or damage caused by virtually any external event during transit, unless specifically excluded. The policy extends across all stages of the journey, including loading, unloading, temporary storage, and the actual flight.

Cargo insurance covers direct physical damage to your goods from accidents, rough handling, or environmental factors during air transport. If turbulence causes pallets to shift and damage fragile electronics, or if forklift operators puncture packaging during ground operations, your policy responds. Water damage from firefighting efforts or exposure to the elements also falls within standard coverage, as does damage from aircraft crashes or emergency landings.

Your policy protects against theft at any point in the supply chain, from the origin warehouse through transit stops to the final delivery point. If a pallet goes missing during transfer at a hub airport or gets stolen from secure storage, you're covered for the full declared value. Complete loss of the aircraft, though rare in air cargo operations, triggers full compensation under the policy terms.

Comprehensive cargo insurance covers what happens to your goods, not just while airborne, but throughout the entire door-to-door journey.

Understanding where your cover stops is just as important as knowing what it protects. Most cargo insurance policies contain standard exclusions that can leave you exposed if you're not paying attention, and some gaps only become visible when you actually need to claim. The difference between comprehensive protection and unexpected liability often comes down to reading the fine print before goods leave the ground.

Your policy typically excludes inherent vice, which means damage caused by the natural characteristics of the cargo itself. If frozen goods thaw because they're temperature-sensitive, or if fruit spoils during a delayed flight, standard insurance won't pay out. You also face exclusions for wilful misconduct by your staff, acts of war, and delays that don't result in physical damage. Loss of market value because goods arrive late, even if intact, falls outside most policies.

Packaging inadequacy represents another common exclusion. If you fail to meet industry packing standards and goods shift during flight, insurers will reject your claim based on insufficient preparation rather than transit risk.

Exclusions aren't designed to catch you out, but they do require you to understand your responsibilities before arranging cover.

Claims fail when you can't prove goods were in sound condition before departure. Without proper pre-shipment inspections, photographic evidence, or third-party surveys, insurers assume damage existed prior to transit. Your declared value must also match actual cargo worth, as underinsurance triggers proportional claim reductions.

Your cargo insurance policy adapts to whichever transport mode you choose, but the underlying principles and coverage mechanics remain consistent across air, sea, and road freight. Each mode carries specific risks that influence premium calculations and the level of scrutiny insurers apply during claims assessment. When cargo insurance explained properly, you'll see that the policy structure stays similar while the risk factors change based on how goods move.

Air freight policies reflect the higher value density and shorter transit times typical of airborne cargo. Insurers charge premiums based on the cargo's declared value, the route's risk profile, and the nature of goods being shipped. You'll typically pay between 0.2% and 0.5% of the cargo value for standard air shipments, with rates climbing for high-risk items like precious metals or sensitive electronics.

The policy activates from the moment your cargo enters the air carrier's custody at the origin airport and continues until final delivery at the destination. Claims processing moves faster for air cargo because transit times are compressed and documentation trails are more precise than with sea or road transport.

Sea freight insurance costs less per shipment due to lower value density but extends over significantly longer periods. Your goods remain at risk for weeks rather than hours, increasing exposure to environmental damage, theft at multiple ports, and handling errors. Road transport policies focus on shorter domestic movements with coverage emphasising theft and road accident risks rather than the broader perils of international ocean shipping.

Different transport modes demand different risk management approaches, but your insurance structure protects cargo value regardless of how goods travel.

When cargo insurance explained in practical terms, the claims process determines whether your policy delivers real protection or just paperwork. You need to act fast when damage or loss occurs, as most policies require notification within 24 to 48 hours of discovery. Your insurer will assign a claims handler who guides you through the submission process, but the quality of your documentation directly impacts how quickly you receive payment.

Your claim requires a complete evidence package that proves both the loss and its value. Start with the original commercial invoice showing what the cargo was worth, followed by the bill of lading or airway bill confirming the shipment details. You'll also need photographs of the damaged goods, a surveyor's report if the loss exceeds certain thresholds, and any correspondence with the carrier about the incident.

Missing documents delay claims for weeks or result in outright rejection. Insurers won't accept verbal explanations when written proof is available, so gather everything before submitting your claim.

Claims succeed or fail based on documentation quality, not on the severity of the loss itself.

Standard claims take two to four weeks to process once you've submitted complete documentation. Simple cases involving clear physical damage settle faster, while total loss claims requiring extensive investigation can extend to several months. Your insurer pays out based on the declared cargo value minus any applicable deductibles, transferring funds directly to your nominated bank account once they approve the claim.

Having cargo insurance explained thoroughly means you now understand the coverage you need, the exclusions to watch for, and how to handle claims when incidents occur. Your next move involves reviewing your current insurance arrangements against the gaps and limitations outlined in this article. Check whether your declared values match actual cargo worth, verify your policies cover door-to-door transit, and confirm you have processes in place to document shipments properly from departure through delivery.

When you're ready to book your next air cargo charter with full technical certainty and transparent pricing, CharterSync provides the digital platform that removes manual guesswork from the process. You'll get instant aircraft matching, confirmed loadability analysis, and real-time tracking for every shipment. Your insurance protects the value, but choosing the right aircraft and operator reduces the likelihood you'll ever need to file a claim in the first place.

.png)